AB-ICI: фундаментальные факторы - Альфа-Банк

advertisement

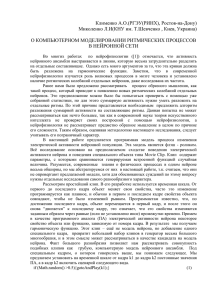

AB-ICI: фундаментальные факторы предопределили снижение Наталия Орлова (+7 495) 795-3677 31 марта 2011 г. www.alfabank.com NOrlova@alfabank.ru Москва Основные выводы • Индекс AB-ICI снизился на 1.8% в прошлом месяце на фоне оттока капитала и слабой макроэкономической статистики • Мы придерживаемся позитивной позиции относительно 2Кв11; рост потребления и инвестиций должен поддержать индекс AB-ICI Снижение индекса AB-ICI на 1.8% в прошлом месяце положило конец тренду роста, начавшемуся в сентябре Отток капитала негативно повлиял на индикатор уверенности в экономике В прошлом году FDI снизились на 13% г/г Рост рынка был ограничен негативными новостями из Японии Индекс AB-ICI потерял в прошлом месяце 1.8% Индекс AB-ICI потерял в прошлом месяце 1.8%, впервые после восстановления индекса, которое началось в сентябре прошлого года. Мы считаем это падение вполне предсказуемой реакцией на слабые фундаментальные тренды: • Индикатор уверенности в экономике вернулся назад к уровню декабря 2010 г. Мы считаем, что основной причиной такого ухудшения является отток капитала: в декабре 2010 г. чистый отток капитала составил $8 млрд, в январе этот индикатор равнялся $11 млрд, а в феврале - $6 млрд. ЦБ ожидает, что отток капитала сохранится в марте и составит $20 млрд за 1Кв11; • Индикатор доверия иностранных инвесторов также снизился, отражая отсутствие восстановления FDI в 4Кв10. В годовом исчислении показатель FDI снизился на 13% г/г, несмотря на то, что российский ВВП вырос на 4% в 2010 году; • Индикатор уверенности в российском рынке остался практически неизменным. Несмотря на рост цен на нефть, негативные новости из Японии существенно повлияли на настроения на рынке. Решение страны повысить налоги в 2012 г., для покрытия убытков от землетрясения, предполагает неблагоприятные последствия для мировой экономики, что ограничивает приток капитала в страны развивающихся рынков, включая Россию. Илл. 1. Индекс AB-ICI снизился на 1.8% в прошлом месяце 6.0 5.0 4.0 3.0 2.0 1.0 фев.11 сен.10 апр.10 ноя.09 июн.09 янв.09 авг.08 мар.08 окт.07 май.07 дек.06 июл.06 фев.06 сен.05 апр.05 ноя.04 июн.04 янв.04 авг.03 мар.03 0.0 Источник: Российская экономическая школа, Отдел исследований Альфа-Банка RESEARCH DEPARTMENT research@alfabank.ru The contents of this document have been prepared by Natalia Orlova of OJSC Alfa Bank ("Alfa Bank") as Investment Research within the meaning of Article 24 of Commission Directive 2006/73/EC implementing the Markets in Financial Instruments Directive (2004/39/EC). Please refer to the further important information in relation to this Document located on the last page. Темпы роста должны улучшиться во 2Кв11 Располагаемый доход снизился в феврале Февраль показал мало улучшений по сравнению с относительно слабой январской макроэкономической статистикой. Реальный располагаемый доход снизился на 1.5% г/г в феврале, а Росстат понизил свою январскую оценку с -5.5% до -5.8% г/г. С учетом уровня безработицы 7.4% - выше уровня 7.2%, зарегистрированного в декабре прошлого года – это предполагает, что конечный спрос может остаться слабым в краткосрочной перспективе, и что рост розничной торговли на 3.3% г/г в феврале не был обусловлен фундаментальными факторами. Восстановление инвестиций попрежнему сдерживается строительством Рост инвестиций несколько восстановился с -4.7% г/г в январе до -0.4% г/г в феврале, но все еще остается под давлением из-за сниженной активности в строительном секторе. Рост в сегменте жилищного строительства составил -6.4% г/г в феврале, в результате чего рост строительства в целом составил всего 0.4% г/г. Рост пенсий на 10% в апреле может позитивно сказаться на потреблении; активность в строительном секторе также должна ускориться Несмотря на негативные индикаторы, мы считаем,. что 2Кв11, скорее всего, принесет хорошие новости. Во-первых, президент Медведев недавно решил поднять пенсии на 10% в апреле вместо двухэтапного повышения в апреле и октябре. Мы считаем, что это поддержит розничную торговлю в мае-июне. Во-вторых, правительство Москвы недавно завершило ревизию планов в области строительства и теперь готово возобновить предоставление финансирования. Рост производства строительных материалов дает нам основания надеяться на скорое восстановление строительного сектора. Рост импорта, % г/г (прав . шк.) -20% -40% -60% янв.11 0% окт.10 0% июл.10 -20% 10% апр.10 1 фев 11 1 янв 11 1 дек 10 1 ноя 10 1 окт 10 1 сен 10 1 авг 10 1 июл 10 1 июн 10 -20% 1 май 10 -10% 20% 20% янв.10 0% 0% производство % г/г окт.09 20% и % г/г июл.09 40% 10% 40% Строительство апр.09 60% 20% Илл. 3. кирпичей янв.09 Илл. 2: Розничная торговля, располагаемый доход и импорт -10% -40% -20% -60% -30% Располагаемый доход, % г/г Произв одств о кирпичей (л.шк.) Розничная торгов ля, % г/г Рост строительств а (пр.шк.) Источник: Росстат, ЦБ, Отдел исследований Альфа-Банка Источник: Росстат, Отдел исследований Альфа-Банка Счет движения капитала долен начать улучшаться в марте после оттока $17 млрд, зафиксированного за 2M11 Мы также ожидаем, что регистрируемый в последнее время сильный отток капитала, который, по оценкам, составил $17 млрд в январефеврале, замедлится в ближайшие месяцы. Мы считаем, что этот отток обусловлен возросшей налоговой нагрузкой: согласно данным правительства, около 400 компаний перенесли свой бизнес в другие страны СНГ, чтобы избежать уплаты социального налога в размере 34%. На наш взгляд, это и является основной причиной того, почему Россия продолжала терять капитал даже после того, как отток в декабре составил $8 млрд, и несмотря на высокие цены на нефть. Ставка рефинансирования осталась без изменений, резервные требования повышены Решение ЦБ повысить резервные требования с 4.5% до 5.5% по иностранным заимствованиям и с 3.5% до 4.0% для внутреннего фондирования является признаком того, что можно ожидать улучшений по счету движения капитала. Тем не менее, регулятор оставил без изменений ставку рефинансирования, поскольку инфляция замедлилась в марте. Годовая инфляция, как ожидается, составит 9.5%, на уровне февраля. Alfa Bank Investor Confidence Index December 29, 2010 2 Contact Information Alfa Bank (Moscow) Head of Equities Telephone Research Department Telephone Head of Research Oil & Gas Macroeconomics Banking Telecommunications, Industrials Utilities Metals & Mining Consumer, Agriculture, Pharmaceuticals Chemicals, Logistics, Industrials Russian Product Editorial Translation Production Equity Sales & Trading Telephone Facsimile International Domestic Institutional th Alfa Capital (Kiev) 77-a Chervonoarmiyska St.(6 floor) Kiev, Ukraine 03150 Research Department Telephone Facsimile Analysts Equity Sales & Trading Sales & Trading Telephone (+380 44) 490-1600 (+380 44) 490-1601 Denis Shauruk, Oleh Yuzefovych Sergey Grigorian, Denis Dolmatov, Yulia Grigoryan (+380 44) 490-1600 th Alfa Capital Markets (London) Telephone Facsimile Telephone (Sales & Sales Trading) Sales Sales Trading Alforma Capital Markets (New York) Sales Trading Fixed Income Sales (+7 495) 795-3676 Peter Szopo Pavel Sorokin, Alexander Bespalov Natalia Orlova, Ph.D., Dmitry Dolgin Jason Hurwitz Iouli Matevossov, CFA, CPA Alexander Kornilov, CFA, Elina Kulieva, Ph.D., Fedor Kornachev Barry Ehrlich, CFA, Maxim Semenovykh, Sergei Krivokhizhin, Ph.D. Alexandra Melnikova, Irina Prokopyeva Georgy Ivanin, Vladimir Dorogov, CFA Angelika Henkel, Ph.D., Alan Kaziev David Spencer, Heather Dean Anna Sholomitskaya, Elena Elovskaya Aleksei Balashov (+7 495) 223-5500, 223-5522 (+7 495) 745-7897 Roland Glasfors, Victoria Duben, Michael Kotov, Dmitry Ryzhkov Dmitry Soloviev, Dmitry Demchenko, Mikhail Babaev, Evgeny Tereschenko (+7 495) 795-3680 Sergey Rybakov, Valeriy Kremnev, Evgeniy Batelman Alfa-Direct Sales Team Telephones Facsimile Sales 12 Akad. Sakharov Prospect, Moscow, Russia 107078 Michael Pijiolis (+7 495) 795-3712 1 Angel Court, 14 Floor, London, EC2R 7HJ (+44 20) 7588-8500 (+44 20) 7382-4170 (+44 20) 7382-4175 Matthew Arnold (+44 20) 7382 4171 Victoria Filimonova (+44 20) 7382-4172 Robert Szucsich (+44 20) 7382-4174 Douglas Babic (+44 20) 7382-4178 1270 Avenue of the Americas, New York, NY 10020 (+1 212) 421-7500 (+1 212) 421-8633 Isai Pochtar (+1 212) 421-8564 Michael Jordan (+1 212) 421-8560 Yan Gloukhovsky (+1 212) 421-8567 Jeffrey Weichsel (+1 212) 421-8563 Copyright Alfa Bank, 2011. All rights reserved. IMPORTANT INFORMATION The contents of this document have been prepared by Open Joint Stock Company Alfa Bank ("Alfa Bank") as Investment Research within the meaning of Article 24 of Commission Directive 2006/73/EC implementing the Markets in Financial Instruments Directive 2004/39/EC ("MiFID"). Alfa Capital Markets ("ACM") is distributing this document to its clients in the EEA and accepts no responsibility towards any other classes of recipient. Alfa Bank and ACM have in place appropriate conflicts of interest policies and procedures aimed at ensuring the objectivity of the information contained in this document. Alfa Bank Group has financial interests in X5, VimpelCom and TNK-BP. X5 is listed on the LSE. VimpelCom is listed on the NYSE. TNK-BP is listed on the RTS Board. This research has been produced independently from all of the above relationships. Note that the recommendations contained in this document may differ materially from recommendations issued by Alfa Bank and distributed by Alfa Capital Markets in the 12 months preceding the publication of this document. The information contained in this document is provided for information purposes only and is not a marketing communication, investment advice or personal recommendation within the meaning of MiFID. The information must not be used or considered as an offer or solicitation of an offer to sell or to buy or subscribe for any securities or financial instruments. In the UK, this document does not constitute a Financial Promotion within the meaning of section 21 of the Financial Services and Markets Act 2000 (as amended). ACM is regulated by the Financial Services Authority (“FSA”) with FSA registration number 416251, for the conduct of UK investment business and is the trading name of the UK branch of Alfa Capital Holdings (Cyprus) Limited (“ACC”), which is authorized by the Cyprus Securities and Exchange Commission under license number CIF 025/04. This document is not for distribution to retail clients as defined by MiFID and may not be communicated to such persons. This document is not for distribution or use by any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation or which would subject Alfa Bank, ACC, ACM or any other group entity to authorization, licensing or other registration requirements under applicable laws. The information contained in this document is the exclusive property of Alfa Bank. Unauthorized duplication, replication or dissemination of this document, in whole or in part, without the express written consent of Alfa Bank is strictly prohibited. Although the information in this document has been obtained from, and is based on, sources Alfa Bank believes to be reliable, no representation or warranty, express or implied, is made by Alfa Bank, ACM or the authors. ACM and its officers and employees do not accept any responsibility as to the accurateness or completeness of any information herein or as to whether any material facts have been omitted. All information stated herein is subject to change without notice. ACM makes no warranty or representation that any securities referred to herein are suitable for all recipients and any recipients considering investment decisions should seek appropriate independent advice. Nothing in this document constitutes tax, legal or accounting advice. Alfa Bank, ACC and their associated companies, officers, directors or employees (excluding any financial analysts or other personnel involved in the production of research), from time to time, may deal in, hold or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to the securities, financial instruments and companies mentioned in this email, or may have been, or may be represented on the board of such companies. If such circumstances arise, ACM, Alfa Bank, ACC and their associated companies have in place appropriate conflicts of interest policies and procedures to ensure that investment research remains independent and objective. A summary of ACC's conflicts of interests policy (which also covers ACM), containing details relevant to investment research, is available upon request from ACC or ACM. ACC and ACM have arranged for Alfa Bank and other relevant group entities involved in the production of research to implement equivalent policies. This document is distributed in the United States by Alforma Capital Markets, Inc., a subsidiary of Alfa Bank, which accepts responsibility for its contents. Alforma Capital Markets, Inc. did not contribute to the preparation of this report and the authors are neither employed by, nor are associated persons of, Alforma Capital Markets, Inc. The issuing entity and authors may not be subject to all of the disclosures and other US regulatory requirements to which Alforma Capital Markets, Inc. and its employees are subject. Any US person receiving this report who wishes to effect transactions in any securities referred to herein should contact Alforma Capital Markets, Inc., not its affiliates. Alfa Bank is incorporated, focused and based in the Russian Federation and is not affiliated with US-based Alfa Insurance.